Your EBITDA Is Strong. But Is Your Business Sellable?

Strong EBITDA is necessary but not sufficient to sell a business — buyers scrutinize the quality and durability of earnings, not just the headline number.

A company with $13M in revenue and $5M in EBITDA failed to sell after a year on the market because two structural risks — 45% revenue dependence on a single distribution channel and 16% revenue from one customer — triggered valuation disputes, and the deal fell apart during due diligence.

A concentrated revenue base, even at strong margins, creates deal risk that sophisticated buyers will find and price against. Businesses where any single customer accounts for 5% or more of revenue, where revenue flows through a single channel or relationship, or where recurring revenue is minimal , face a high likelihood of a buyer wanting to renegotiate the deal during due diligence. A professional market assessment — reviewing financials, revenue composition, customer concentration, and competitive positioning — is the critical first step before going to market, and is the most reliable way to avoid surprises that kill deals.

— Rich Jackim, Jackim Woods & Co.

Your EBITDA Is Strong. But Is Your Business Sellable?

Every business owner considering selling their business deserves a clear-eyed assessment of one foundational truth: EBITDA is a critical metric, but it does not tell the complete story. Owners who discover this after months of trying to sell their business — or after a deal fails during due diligence — will have wasted a lot of time and money.

The following is a situation we have seen multiple times in our practice. The details have been modified for confidentiality, but the dynamics are real—and offer important insights for any owner thinking about an exit.

A Business That Looked Great on Paper

Last year, we spoke with the owner of a business services company who had spent twenty years building his business. Now 65, he was ready to retire and sell the company. The financial profile was attractive: approximately $13 million in revenue with $5 million in EBITDA – strong margins that would get buyers’ attention.

Early in the process, the owner’s CPA reviewed the financials and told the owner the company was probably worth $25 million – exactly what the owner wanted to hear. The CPA explained that the EBITDA was there, and in his experience, companies like this one sold for 5x EBITDA. The owner felt confident, so he hired an M&A advisor to sell the business. After a year on the market, two buyers had withdrawn their offers during due diligence, and the business was still not sold.

Strong EBITDA opens doors. But what buyers find when they look inside determines whether a deal actually closes.

What the Financial Analysis Revealed

When buyers started their due diligence, they discovered the company’s revenue composition contained concentration risks that ultimately derailed the deal:

45%Revenue from One Distribution Channel |

16%Revenue from a Single Customer |

61%Revenue Concentration Risk |

Revenue channel concentration: 45% of total revenue was generated through a single distribution channel, a key salesperson, who was the same age as the business owner. While that salesperson had performed reliably for years, the fact that the company depended on someone so close to retirement age was a structural dependency that concerned sophisticated buyers.

Customer concentration: 16% of revenue was attributable to one customer, a large manufacturer with multiple locations. This indicated a customer concentration issue that affected lending eligibility and the buyer’s financing options, which in turn affected the overall risk profile of the deal.

These were not deal killing factors individually. But collectively, they represented risks that sophisticated buyers identified in due diligence, and in one case, used to try to negotiate a huge valuation adjustment (50%) — or in the other case, as grounds to exit the process entirely.

When Market Conditions Validated a Buyer’s Analysis

What ultimately killed the deal was during due diligence, an external event occurred that demonstrated precisely why concentration risk demands early attention.

The company received formal notification that its largest customer — representing 16% of annual revenue — had been acquired by a direct competitor. As part of the acquirer’s vendor consolidation strategy, they provided notice that they would be scaling back their purchase orders over the next six months, with the goal of consolidating all purchase orders with the new parent company’s vendors.

The impact was immediate and material. Sixteen percent of the company’s revenue had just disappeared and could not easily be replaced. The seller’s valuation and negotiating position was now fundamentally changed by a single event outside of their control. This is exactly what buyers feared, and it had come true.

The Strategic Lesson for Owners Selling Their Businesses

Advisors who do not earn success fees when a transaction closes have limited incentive to tell clients the hard honest truth about their client’s business. The result is that business owners often try to sell their business without a clear understanding of how buyers will evaluate their company — and without the opportunity to fix those risk factors before they become deal killers.

As the above example demonstrates, EBITDA matters a lot. But experienced buyers will also be looking at the quality and durability of those earnings:

- Does any single customer represent more than 5% of a company’s revenue?

- Is revenue dependent on a single channel, platform, or relationship that could be disrupted?

- Is revenue generated from one product or service, or diversified over a wide range of products and services?

- Is there industry concentration risk with services or products serving only one industry?

- How much of the revenue base is genuinely recurring, contracted, or relationship-protected versus transactional?

- How is the business positioned relative to industry transformation — as an adopter or as a laggard?

- How would EBITDA be affected if the single largest customer or channel relationship were impaired?

These are the questions that determine whether reported EBITDA represents durable, transferable earnings—or a business that will be systematically discounted during the diligence and negotiation process.

The Question Every Owner Should Ask Before Selling Your Business

The Question Every Owner Should Ask Before Selling Your Business

It is not simply “What is my EBITDA?”

The more important question is: “Do my revenue and EBITDA accurately reflect the risk-adjusted financial performance of my business?”

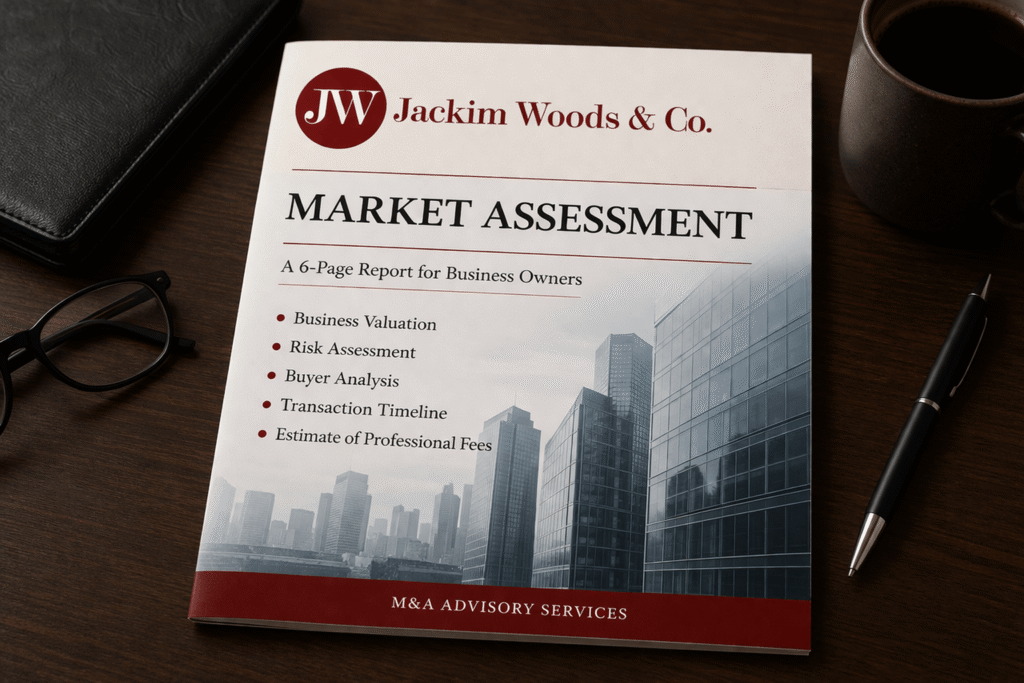

That is precisely what a professional market assessment and business valuation is designed to answer. Not to produce an optimistic number, but to give you the honest, complete picture that enables you to maximize transaction value and approach the market from a position of knowledge rather than a host of assumptions.

Why a Free Market Assessment Increases Your Options when Selling Your Business

At Jackim Woods & Co., our complimentary market assessments are designed to give business owners the analytical foundation they need before making one of the most consequential financial decisions of their lives.

We review of your financials, revenue composition, customer and channel concentration, competitive positioning, and provide you with the realistic range of values a qualified buyer would assign to your business. It means identifying the factors that could affect a transaction — and giving you to option to address them before you go to market.

Business owners who understand their true market value make better decisions: about timing, about preparation, about which buyer profiles to target, and how to position the company’s story. They do not spend months pursuing a process that was unlikely to succeed. And they are not surprised by what buyers find.

If you are considering a sale — even if your timeline is one to three years out — an objective assessment of where your business stands today is the most valuable step you can take.

Please note: Because of the time and effort that goes into to preparing a market assessment, free market assessments are only available for businesses generating at least $5 million in revenue or $1 million in EBITDA.

About Jackim Woods & Co.

Rich Jackim is an investment banker, entrepreneur, and former mergers and acquisitions attorney.

Rich Jackim is an investment banker, entrepreneur, and former mergers and acquisitions attorney.

For the last 25 years, Rich has been providing boutique investment banking services to small and lower middle-market companies in a wide range of industries across the United States and Canada.

Rich also founded a successful training and certification company called the Exit Planning Institute, which he sold to a private equity group in 2012.

Rich is also the author of the critically acclaimed book, The $10 Trillion Dollar Opportunity: Designing Successful Exit Strategies for Middle Market Businesses.

Jackim Woods & Co offers skilled mergers and acquisitions advisory services to privately companies in both sell-side and buy-side transactions. Jackim Woods & Co has arranged over 120 successful transactions, ranging from one million to more than eighty million dollars in value.

If you own a business and are interested in exploring your options, I would welcome an opportunity to speak with you.

Feel free to contact me at 224-513-5142 or rjackim@jackimwoods.com.

Read More

America’s $5 Trillion Business Ownership Crisis

America is facing a business ownership crisis: 6 million small businesses will need new owners by 2035, and according to a McKinsey study titled The Great Ownership Transfer, 92% will simply close rather than sell.

The businesses most at risk have revenues between $1 million and $10 million — owner-operated firms spanning business services, regional manufacturing, and B2B specialties that are too small for institutional private equity and too complex for Main Street brokers. Together, they represent up to $5 trillion in enterprise value that will largely disappear unless buyers and sellers find each other in time. Rich Jackim predicted this wave in 2007 and co-founded the Exit Planning Institute to address it, training over 9,000 Certified Exit Planning Advisors — yet the majority of business owners still exit without a plan. For sellers, the window to transact at full value is narrowing every year; for buyers, the opportunity to acquire profitable, established businesses at reasonable prices has never been larger.

— Rich Jackim, Jackim Woods & Co.

McKinsey & Company just published a study that deserves attention from every business owner and serious business buyer in the country. The study, titled The Great Ownership Transfer, puts hard numbers to something I’ve been saying for nearly two decades: America is approaching a massive, largely unaddressed transition of business ownership — and most business owners aren’t ready for it.

The headline finding: 6 million small businesses will need new owners by 2035 as Baby Boomers retire. The sad news is that, according to McKinsey, 92% of these will not be sold and will simply shut their doors. The good news is that this means at least 1 million are viable acquisition targets, representing up to $5 trillion in enterprise value.

I Saw This Coming in 2007

When I wrote the critically acclaimed book, The $10 Trillion Opportunity, this demographic wave was already clearly on the horizon. The math was never complicated: the largest generation of entrepreneurs in American history, the Baby Boomers, would eventually retire, and the buyer infrastructure to acquire these lower-middle-market businesses was not well developed.

When I wrote the critically acclaimed book, The $10 Trillion Opportunity, this demographic wave was already clearly on the horizon. The math was never complicated: the largest generation of entrepreneurs in American history, the Baby Boomers, would eventually retire, and the buyer infrastructure to acquire these lower-middle-market businesses was not well developed.

That book led me to co-found the Exit Planning Institute, and to create the Certified Exit Planning Advisor (CEPA) designation — a program that has now trained more than 9,000 graduates and helped establish exit planning as a recognized professional discipline. Entire conferences, curricula, and consulting practices have been built around it.

And yet — despite all of that progress — the majority of business owners still exit without a plan in place. The McKinsey data makes that painfully clear: 92% of small business exits or sales today will end in closure. Not sale. Not succession. Closure. Let that sink in.

Profitable companies with real customers, trained employees, and decades of hard-earned reputation — simply shutting their doors because no qualified buyer stepped forward in time.

The Forgotten Core of the American Economy

The businesses most exposed to this risk share a common profile: revenues between $1 million and $10 million, spanning business service providers, regional manufacturers, and B2B specialists. These are owner-operated firms that have quietly powered local economies and supply chains for decades.

They’re too small to attract institutional private equity. Too complex for Main Street business brokers. And too often overlooked by the buyers who could give them a real future. It’s a structural gap hiding in plain sight — and it’s where the closure problem is most acute.

What This Means for Buyers & Sellers

Here’s the other side of the equation that doesn’t get discussed enough.

We talk with a lot of prospective buyers every day. And while well-run businesses with strong fundamentals cross our desk regularly, most buyers aren’t in the market for a good company. They’re searching for the right one — the one that checks all the boxes, including the right combination of timing, fundamentals, and transformative upside.

The challenge is that “right” means different things to different buyers. The right fit depends on the buyer’s background, industry experience, capital structure, growth thesis, and risk tolerance. That means if you are buyer, finding your right acquisition or isn’t a passive exercise. The same applies if you are a seller. It requires extensive, targeted research and outreach — two things we do every day.

The Bottom Line

This is precisely the space that Jackim Woods & Co. was built to serve. Paul, Jim, and I have spent years developing the relationships, the methodology, and the market intelligence to move these businesses from owner-operated to professionally transitioned — without watching them quietly disappear.The Great Ownership Transfer is not a future event. It’s happening now. Every year that passes without a transaction plan is a year closer to a closure that didn’t have to happen.

If you’re a business owner thinking about your exit — whether in two years or ten — the time to start the conversation is now, before urgency forces your hand.

Contact us at Jackim Woods & Co. We’re happy to help you explore your options, help you develop a plan, and help you find the right buyer for your business. Reach us at jackimwoods.com or contact Rich directly to start the conversation.

Read More

The CDL Mill Crackdown: What It Means for the Industry’s Future

The CDL Mill Crackdown: What It Means for Trucking, Safety, and the Industry’s Future

In February 2026, federal investigators fanned out across all 50 states in one of the most aggressive enforcement actions the trucking industry has ever seen. Over the course of just five days, the Federal Motor Carrier Safety Administration deployed more than 300 investigators and conducted over 1,400 on-site sting operations targeting commercial driver’s license (CDL) training schools. The results were striking: 448 schools received formal notices of removal for failing to meet basic safety standards, and 109 others voluntarily withdrew from FMCSA’s national Training Provider Registry the moment they learned investigators were on their way. Another 97 remain under active investigation.

Combined with earlier enforcement waves — including the removal of nearly 3,000 providers in December 2025 and another 3,800 in January 2026 — FMCSA has now purged more than 7,000 CDL schools from its registry since 2025. To put that in context, the registry listed roughly 40,000 training providers before the crackdown began, meaning the purge has touched nearly one in five listed schools. It’s worth noting that many of the first wave of removals were inactive operators — school districts, community colleges, and small fleets that had registered but hadn’t trained a driver in years. The February 2026 sting was more significant precisely because it targeted active operators who were actively credentialing drivers. Transportation Secretary Sean Duffy framed it plainly: “For too long, the trucking industry has operated like the Wild, Wild West.”

Combined with earlier enforcement waves — including the removal of nearly 3,000 providers in December 2025 and another 3,800 in January 2026 — FMCSA has now purged more than 7,000 CDL schools from its registry since 2025. To put that in context, the registry listed roughly 40,000 training providers before the crackdown began, meaning the purge has touched nearly one in five listed schools. It’s worth noting that many of the first wave of removals were inactive operators — school districts, community colleges, and small fleets that had registered but hadn’t trained a driver in years. The February 2026 sting was more significant precisely because it targeted active operators who were actively credentialing drivers. Transportation Secretary Sean Duffy framed it plainly: “For too long, the trucking industry has operated like the Wild, Wild West.”

He’s not wrong. And from an investment banker’s perspective, the scale of the problem these actions are addressing is even larger than the headlines suggest.

What CDL Mills Actually Are

A CDL mill is a training provider that collects tuition fees, issues completion certificates, and does little else of value. Investigators found schools operating out of fake addresses, using unqualified instructors, training students on vehicles that didn’t match the license class being sought, and in many cases simply selling passing scores to anyone who could pay.

The documented fraud runs deep. Between 2001 and 2025, DOT Office of Inspector General investigations conservatively estimated that over 6,000 fraudulent licenses were issued to drivers who couldn’t operate the vehicles they were credentialed to drive. In Massachusetts, a former State Police sergeant ran a scheme for years, arranging passing scores for dozens of applicants he privately described as “brain dead” and people who “should have failed about 10 times already” — and the scheme continued operating for more than a year after federal Entry-Level Driver Training rules went into effect in 2022. In Louisiana, a federal grand jury indicted multiple state motor vehicle employees for bribery. In Florida, a Russian-language trucking school charged students up to $5,000 for guaranteed CDLs, complete with covert cameras and wireless earpieces to feed answers during tests.

These weren’t isolated incidents. They represent a market that grew precisely because it was profitable and, for years, essentially unpoliced. From 2022 through 2024, despite widespread complaints, FMCSA removed only four providers from the registry under routine enforcement — three of those for emergency-level violations. The self-certification model that governed CDL training was, in practice, an honor system with no honor.

The Economic Damage Is Real and Measurable

For those of us who work in transportation M&A, the downstream consequences of this fraud show up directly in deal economics — and they are not small.

Experior Logistics

Insurance costs have spiraled industry-wide. The trucking sector has absorbed dramatic liability premium increases over the past decade, driven in significant part by large jury verdicts tied to crashes involving undertrained drivers. Primary liability insurance for owner-operators running under their own authority now reaches $14,000 to $22,000 annually per truck — a cost structure that pressures margins and makes capital formation harder for smaller carriers. When a carrier unknowingly hires a driver whose credentials were purchased rather than earned, it inherits catastrophic liability exposure that may not surface until a fatal accident triggers litigation.

The accident data is damning. In 2023, over 153,000 highway truck accidents resulted in more than 5,400 fatalities — a 40% increase from 2014 levels. The odds of being killed by a commercial truck are now roughly 20 times greater than dying in a commercial airline crash, a disparity that reflects the vast difference in training standards between the two industries. In Fort Pierce, Florida, a driver who could neither speak nor read English obtained a fraudulent CDL and subsequently killed a family of three. In California, a driver whose license was obtained through a bribery scheme triggered a 74-vehicle pileup that killed two people and injured 51 others.

The “driver shortage” narrative was partly manufactured. The Owner-Operator Independent Drivers Association has argued forcefully that CDL mills fueled a “destructive churn” built on a false narrative of a nationwide truck driver shortage. Rather than addressing retention problems and working conditions, some carriers and training operators chose to flood the market with undertrained, low-cost labor — depressing wages for qualified professional drivers and distorting the supply-demand dynamics that buyers and sellers need to accurately price risk. For anyone underwriting a trucking acquisition, a workforce seeded with paper drivers represents unquantified liability hiding in plain sight on the balance sheet.

Valuation integrity was compromised. When a carrier’s safety rating, claims history, and insurance profile reflect the consequences of fraudulent driver credentialing, it directly impairs enterprise value — often in ways sellers themselves don’t fully understand until a buyer’s diligence team starts pulling driver qualification files.

Why the Enforcement Action Is Genuinely Good News

The federal crackdown is disruptive in the short term. Some legitimate drivers trained at now-decertified schools face credentialing complications. Some carriers will need to requalify portions of their workforce. These are real costs.

But the long-term benefits are substantial — and they flow to every honest participant in the industry.

For consumers and the public, the benefit is direct: fewer undertrained drivers on the road means fewer preventable deaths. Enforcement finally aligns regulatory action with a decade of worsening accident statistics.

For employers and carriers, a cleaner training registry reduces the risk of unknowingly inheriting fraudulent credentials. It also strengthens the defensibility of hiring decisions in litigation — a factor that matters enormously when nuclear verdicts can exceed policy limits by multiples. Carriers that have invested in rigorous training pipelines will find those investments increasingly rewarded in both insurance pricing and competitive differentiation.

For the industry’s investment profile, regulatory clarity and improved safety metrics will gradually reduce the liability discount that buyers and insurers apply to trucking assets. Lower accident frequencies, cleaner CSA scores, and a more professionalized driver workforce all improve the risk-adjusted attractiveness of transportation businesses. A cleaner registry should also help normalize insurance markets distorted by years of adverse loss experience — ultimately lowering the cost of capital across the sector.

For legitimate training providers, the removal of competitors who were undercutting the market on price while externalizing costs onto the public restores competitive balance. Schools that invested in qualified instructors, proper equipment, and genuine curricula can now compete on a level playing field.

The Bottom Line

CDL mills are fraud enterprises that monetized a regulatory blind spot while transferring enormous costs onto the public, onto legitimate industry participants, and onto the victims of preventable crashes. The scale of the federal response — more than 7,000 schools removed or flagged out of roughly 40,000 registered providers — reflects how thoroughly that blind spot was exploited.

For investors, buyers, and sellers in the trucking space, the era of treating driver credentialing quality as a back-office compliance matter is over. The cleanup is long overdue. And while the short-term disruption is real, the foundation being laid is one that serious operators, acquirers, and lenders should welcome.

Thinking About Buying or Selling a CDL Training Business?

The regulatory reset underway in the CDL training sector is creating real M&A opportunity — but navigating it requires an advisor who understands both the industry dynamics and the deal mechanics.

The regulatory reset underway in the CDL training sector is creating real M&A opportunity — but navigating it requires an advisor who understands both the industry dynamics and the deal mechanics.

At Jackim Woods & Co., we bring deep expertise in transportation services M&A to every engagement. We understand how FMCSA compliance history, Training Provider Registry status, student completion rates, and instructor credentialing translate into enterprise value — and how buyers and lenders are pricing those variables right now. For sellers, that knowledge means positioning your business to command the best possible outcome in a market that is actively rewarding well-run, compliant operators. For buyers, it means identifying acquisition targets with clean regulatory profiles and durable competitive advantages before the broader market catches on.

The shakeout created by federal enforcement is far from over. Owners of legitimate, compliant CDL training businesses may find that this is an exceptional time to explore a sale, recapitalization, or strategic partnership. Acquirers looking to build scale in a consolidating market have a narrowing window to act before valuations fully reflect the new competitive landscape.

Whether you are a CDL school owner weighing your exit options or a strategic buyer looking to enter or expand in the training sector, we would welcome the opportunity to discuss what your business is worth and what the market looks like today.

Contact us for a free, no-obligation conversation.

Rich Jackim, Managing Director Jackim Woods & Co. www.jackimwoods.com

Rich Jackim is Managing Director of Jackim Woods & Co., a lower middle market M&A advisory firm, and author of The $10 Trillion Opportunity. The firm advises owners and acquirers across transportation, distribution, and business services.

Read More