Calculating the Pre-Money Value of an EdTech Company

What Is a Pre-Money Valuation?

One of the first questions I get from potential clients is how do you calculate the pre-money value of an EdTech company.

A pre-money valuation refers to the value of a company before it receives any external funding from investors. Put another way; a pre-money valuation is how much a company is worth before you start your capital raise. Angel investors and venture capital firms use a company’s pre-money value to determine what their investment in the company is worth.

Key Points

- A pre-money valuation is the value of an EdTech company before it receives an investment from an external investor.

- Potential investors use a company’s pre-money value to determine its worth before investing in it.

- Post-money valuations are different from pre-money valuations. A post-money valuation estimates a company’s value after it receives funding.

- This article was written for founders and managers of EdTech companies, but the same concepts apply to any business seeking angel investors or venture capital funding.

Understanding Pre-Money Valuation

Pre-money is the valuation of a company before a round of financing and gives investors a picture of the company’s current value. Pre-money values are determined before each round of funding a company receives. You can and should re-evaluate your pre-money valuation each time you seek seed, angel, Series A, B, or C round of venture funding.

How To Calculate a Pre-Money Valuation

The management team of the company seeking funding typically proposes a pre-money valuation to potential investors. However, “value is in the eye of the investor,” so each potential investor will have their own idea of the company’s pre-money valuation.

Calculating the pre-money valuation for a company is pretty straightforward. Here’s the basic formula:

Pre-Money Valuation = Post-Money Valuation – Investment Amount

So, if an EdTech company’s post-money valuation is $30 million after receiving a $10 million investment has a pre-money valuation of $20 million.

As you can see, a company’s pre-money valuation is heavily dependent on the company’s post-money valuation, so I encourage you to read my article “How to Value an EdTech Company: Multiples & Example.” In that article, I describe in-depth how to calculate a company’s post-money valuation and provide real-world multiples and an example.

Remember that the pre-money valuation is the basis for determining the amount of funding that investors are willing to provide and how much of the company’s equity they want in return. The company’s management team might propose one value and talk to dozens of potential investors before finding an investor who agrees with the company’s estimate of value. In most cases, the actual pre-money valuation used is heavily negotiated between the investors and management.

Things to Consider

First, remember that an EdTech company’s pre-money valuation is not a static number. That means it can and does change day by day. That’s because a company’s post-money valuation, and hence its pre-money valuation, are affected by general market demand, the public stock market, interest rates, investor appetites, and the company’s performance.

Next, remember that a pre-money valuation is done before each round of funding a company seeks. The pre-money value of an EdTech business will change based on the financing round (i.e, risk level), performance of the company, and market conditions. If a company is growing nicely and hitting its targets, its pre-money value should increase with each financing round, despite the increased investment required.

Third, remember that a pre-money valuation is still possible on early-stage EdTech companies that are pre-revenue, meaning the company has not generated any sales yet. In a pre-revenue company, investors will base its pre-money valuation on a combination of other value factors, including valuations of comparable businesses, projections, growth rates of similar companies, etc. Investors often use insider knowledge of the revenue and market potential of other more established, mature companies in the same sector or that have a similar business model to predict how successful a company will be.

Fourth, even if your EdTech company claims it has created a new industry with new unique solutions, and a new business model, investors will still calculate its value based on the businesses they already know.

Fifth, investors often say, “we invest in people, not companies,” and that’s true. The pre-money valuation of your EdTech company will be greatly affected by the experience and track record of its founders and management team and the likelihood that they will deliver on their promises.

Post-Money vs. Pre-Money Valuations

As its name implies, a post-money valuation differs from a pre-money value because it indicates how much a company is worth after receiving an investment.

To calculate the post-money valuation, please see my article “How to Value an EdTech Company: Multiples & Example.” In that article, I show you how to calculate the post-money value of your EdTech company, so you can figure out how much money you can potentially raise from investors.

Example of Pre-Money Valuation

In that article, I used an example of an EdTech company that determined it had a post-money value of $2.3 million. I also assumed that management projected it needed $1 million in seed money from investors to hit its revenue goals and achieve its exit value.

So, if we assume that the post-money valuation is $2.3 million and the company needs $1 million in seed money, that implies the founders and management team will potentially need to give up 44% of their equity to raise $1 million in growth capital.

That also implies the company’s pre-money value is $1.3 million, because, as we learned above, the pre-money value of your business is calculated as follows:

Pre-Money Value = Post-money value – Investment Amount

$1,300,000 = $2,300,000 – $1,000,000

Understanding the relationship between pre-money and post-money values is important because it allows founders, management teams, and investors to calculate how much equity needs to be given up to incentivize an investor to invest.

About the Author and Jackim Woods & Co.

Rich Jackim is an education industry investment banker and educational industry entrepreneur, and former mergers and acquisitions attorney.

Rich Jackim is an education industry investment banker and educational industry entrepreneur, and former mergers and acquisitions attorney.

For the last 25 years, Rich has been providing boutique investment banking services to middle-market companies in the education sector.

Rich also founded a successful training and certification company called the Exit Planning Institute which he sold to a private equity group in 2012.

Rich is also the author of the critically acclaimed book, The $10 Trillion Dollar Opportunity: Designing Successful Exit Strategies for Middle Market Businesses.

Jackim Woods & Co offers skilled mergers and acquisitions advisory services to privately owned schools, colleges, and EdTech companies in both sell-side and buy-side transactions. Jackim Woods & Co has arranged over 100 successful transactions, ranging from less than one million to more than eighty million dollars in value.

If you own an education-related business and are interested in exploring your options, I would welcome an opportunity to speak with you. Feel free to contact me at 224-513-5142 or rjackim@jackimwoods.com.

Read More

How to Value an EdTech Company: Multiples & Example

One of the hardest things to do when building an EdTech business is determining its value. Whether you are seeking growth capital or looking to exit, you need to have a basic idea of what your business is worth. If you value your business too high, investors won’t be willing to speak with you. If you value it too low, you leave money on the table or end up giving away too much equity to raise the growth capital you need. So, how do you calculate a reasonable value for your EdTech company?

Well, the valuation methodology outlined below applies to all EdTech companies, regardless of when you are pre-revenue, established, or looking to exit.

How to Value an Edtech Company: Multiples & Example

The global Edtech industry is expected to reach a market value of over $340 billion by 2025. Because of strong underlying market trends, the Edtech sector has received some of the highest tech valuations, with publicly traded EdTech companies trading at 5.0x to 18x next twelve months’ revenue (NTM)! These valuations dropped significantly in late 2021 and early 2022, but are expected to rebound. See our article on EdTech multiples.

If you are the founder of an EdTech company and are thinking of raising a round of growth capital, you’re at the right place. In this article, I’ll provide a step-by-step guide on valuing any Edtech company.

First and foremost, it’s important to understand that EdTech companies are not valued like traditional businesses. Valuations of conventional businesses are based on the company’s free cash flow. With EdTech companies, the most common valuation method is what’s referred to as the Venture Capital approach, which values companies based on a multiple of revenues.

In this article, we’ll use publicly-traded companies in the Edtech industry for comps so you can follow along and use them to value your EdTech business.

Note: If you need help preparing a pitch book for investors, contact us to learn how we can help you prepare a solid Edtech pitch book that will significantly increase the odds of a successful capital raise.

Venture Capital Edtech Valuation Method

There are several startup and early-stage valuation methodologies. While none of them is perfect, they all try to estimate a valuation for a business based on several qualitative and quantitative factors. The Venture Capital Valuation Method is the most common method investors use to value Edtech companies.

The VC method considers business fundaments, market demand, and investor return on investment factors.

Why Do Investors Use the Venture Capital Method to Value an EdTech Company?

The VC method is a relatively simple and straightforward way to value an early-stage EdTech company because it is driven by several factors that can be grouped into 4 categories.

1. Market Demand

Your EdTech company will be more valuable if you demonstrate that it is part of a large, highly fragmented market that is growing at double or triple digits.

2. Market Fit & Adoption

Your EdTech company will be more valuable to investors if you prove that the business has early adopters or users (market-fit) and that people are willing to pay for your service (adoption.)

3. Management Team & Track Record

Your Edtech company will be more valuable to investors if you demonstrate that your management team has relevant sector experience and a successful track record of growing similar businesses.

4. Investor’s Expectations & Founder’s Negotiating Power

Last but not least, keep in mind that investors are willing to back EdTech startups and early-stage companies because they can earn a substantial return on their investment. If a startup is deemed too expensive, it reduces an investor’s return on investment, and they won’t invest.

At the same time, the more investors you can pitch to and the more term sheets you receive, the better your negotiating position and the higher the valuation.

The Three Value Drivers When Valuing an EdTech Company

The VC method allows founders and investors to estimate an EdTech company’s value by inputting three main variables:

1. Projected Revenues

Projected revenues are usually based on an integrated financial model that includes projected revenue for the next five years. Keep in mind that unless your financial model, and the assumptions that drive it, are supported by facts and hard data, investors will take them with a grain of salt. So it’s important to work with an independent, objective financial advisor who can help you develop a rock-solid set of projections.

2. Comparable Industry Valuation Multiples

Investors rely heavily on valuation multiples from comparable companies within the same industry and sector. The most common multiple used is EV/Revenue, which stands for Enterprise Value as a multiple of Revenue. See below for 2022 public Edtech company valuation multiples.

These multiples change daily and are sensitive to many variables, including interest rates, stock market performance, IPO results, M&A activity, market demand, etc.

3. Investors’ Required IRR

The other important variable is the rate of return investors are looking for. An investor’s required IRR (“Internal Rate of Return”) depends on the type of investor, the EdTech company’s stage, and the investment’s perceived risk. The higher the perceived risk, the higher the required IRR. For example, an investor would need a higher IRR for a seed money investment in an EdTech startup than for an investment in an early-stage EdTech company looking for a Series A or Series B round of financing.

Edtech Valuation Example

Now that we’ve covered how the Venture Capital valuation method works let’s see how to use it to value an early-stage Edtech company looking to do a Series A capital raise.

Prove Market Fit & Adoption

The first thing to do is create a detailed, integrated financial model that includes historical financial data and operating metrics. This is important because your historical performance will prove market fit & adoption and support the assumptions you use to create your projections.

Expected Revenues

The next step is to create detailed revenue and expense projections for five years. While the valuation is based on a multiple of revenues, it’s also important to know your operating and growth assumptions to determine how much capital you need to raise to hit your revenue targets.

Need help building an integrated financial model and projections? Contact us for a free, no-obligation consultation.

So, for this example, let’s assume your EdTech company is in the K12 reading sector. You’ve been in business for three years and have been funded by personal funds and friends and family investors. Your business now has 450 subscribers and is generating $250,000 in revenue, and your subscriber base grew by 100% last year. You built an integrated financial model with historical results and projected revenue for the next 5 years. The projections show that next year you expect revenues to be $625K and grow to $4.1 million in Year 5.

Below is a very basic example of projected revenues for the next five years.

|

Period |

Revenue | Growth Rate |

| Base |

250,000 |

|

| Year 1 |

625,000 |

250% |

| Year 2 |

1,250,000 |

200% |

| Year 3 |

2,187,500 |

175% |

| Year 4 |

3,281,250 |

150% |

| Year 5 |

4,101,563 |

125% |

| Total |

11,445,313 |

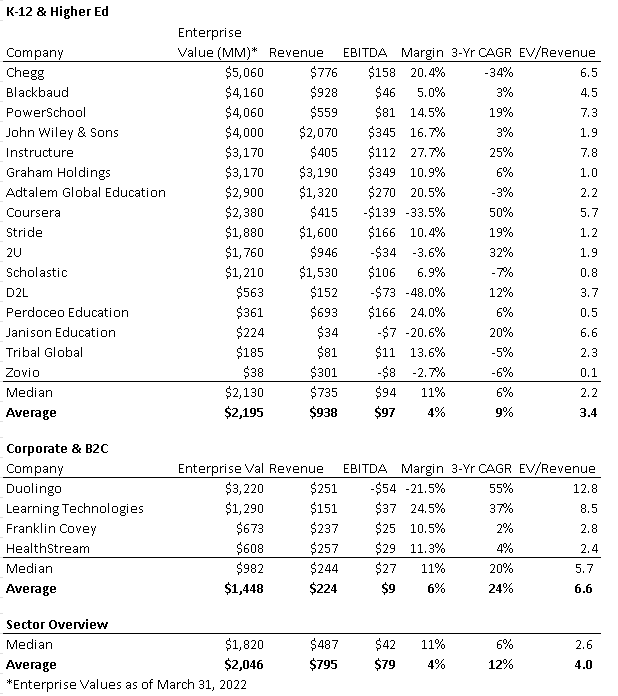

Public EdTech Valuation Multiples

The next step is determining the right multiple to use to value your business.

Investors track over a dozen publicly traded Edtech companies to gauge the market’s appetite for EdTech investments.

While the multiples vary a lot from company to company, each is based on investors’ assessments of the company’s market demand, business model, management team, growth rate, and profitability.

Below is a sample of some of the public EdTech companies we track. Be sure to read this excellent article from the venture capital group, GSV Ventures regarding the valuation of publicly traded EdTech companies.

|

Public EdTech Valuation Multiples |

||||||

| K-12 & Higher Ed | ||||||

| Company | Enterprise Value (MM)* | Revenue | EBITDA | Margin | 3-Yr CAGR | EV/Revenue |

| Chegg |

$5,060 |

$776 | $158 | 20.4% | -34% | 6.5 |

| Blackbaud |

$4,160 |

$928 | $46 | 5.0% | 3% |

4.5 |

| PowerSchool |

$4,060 |

$559 | $81 | 14.5% | 19% |

7.3 |

| John Wiley & Sons |

$4,000 |

$2,070 | $345 | 16.7% | 3% |

1.9 |

| Instructure |

$3,170 |

$405 | $112 | 27.7% | 25% |

7.8 |

| Graham Holdings |

$3,170 |

$3,190 | $349 | 10.9% | 6% |

1.0 |

| Adtalem Global Education |

$2,900 |

$1,320 | $270 | 20.5% | -3% |

2.2 |

| Coursera |

$2,380 |

$415 | -$139 | -33.5% | 50% |

5.7 |

| Stride |

$1,880 |

$1,600 | $166 | 10.4% | 19% |

1.2 |

| 2U |

$1,760 |

$946 | -$34 | -3.6% | 32% |

1.9 |

| Scholastic |

$1,210 |

$1,530 | $106 | 6.9% | -7% |

0.8 |

| D2L |

$563 |

$152 | -$73 | -48.0% | 12% |

3.7 |

| Perdoceo Education |

$361 |

$693 | $166 | 24.0% | 6% |

0.5 |

| Janison Education |

$224 |

$34 | -$7 | -20.6% | 20% |

6.6 |

| Tribal Global |

$185 |

$81 | $11 | 13.6% | -5% |

2.3 |

|

Zovio |

$38 | $301 | -$8 | -2.7% | -6% |

0.1 |

| Median |

$2,130 |

$735 | $94 | 11% | 6% |

2.2 |

| Average |

$2,195 |

$938 | $97 | 4% | 9% |

3.4 |

| Corporate & B2C | ||||||

| Company | Enterprise Value (M)* | Revenue | EBITDA | Margin | 3-Yr CAGR | EV/Revenue |

| Duolingo |

$3,220 |

$251 | -$54 | -21.5% | 55% |

12.8 |

| Learning Technologies |

$1,290 |

$151 | $37 | 24.5% | 37% |

8.5 |

| Franklin Covey |

$673 |

$237 | $25 | 10.5% | 2% |

2.8 |

| HealthStream |

$608 |

$257 | $29 | 11.3% | 4% |

2.4 |

| Median |

$982 |

$244 | $27 | 11% | 20% |

5.7 |

| Average |

$1,448 |

$224 | $9 | 6% | 24% |

6.6 |

| Sector Overview | ||||||

| Median |

$1,820 |

$487 | $42 | 11% | 6% |

2.6 |

| Average |

$2,046 |

$795 | $79 | 4% | 12% |

4.0 |

|

*Data and Enterprise Values |

||||||

In our example of the VC valuation method, we will use the Sector Average EV/Revenue multiple of 4.0.

Keep in mind that when preparing a valuation of your EdTech company, it’s important to select the comparable companies that are the most like the company you are trying to value. That won’t always be possible, but to support your valuation, you’ll need to explain to investors why you selected the comparable companies you picked rather than others.

Adjusting the Multiple for a Private EdTech Company

Because we started with valuation multiples from public companies, we need to adjust that multiple to reflect that your EdTech company is privately owned. Privately owned companies are less valuable than publicly traded companies because they are much more difficult, time-consuming, and expensive to sell. As a result, investors apply an Illiquidity Discount, also referred to as a Discount for Lack of Marketability, of between 20% and 30%.

Let’s use a 25% discount, which results in an adjusted EV/Revenue multiple of 3.0x.

Determining Your Exit Value

The next step in the VC Method is to calculate your EdTech company’s value when your investors exit. In this example, we assumed the exit would be after five years. This is called the Exit Value.

Exit Value = EV/Revenue x Revenue at exit (Year 5)

Year 5 Revenue = $4.1 million

EV/Revenue Multiple = 3.0x

Exit Value = 3.0x x $4.1 million

Exit Value = $12.3 million

Investors’ Required Rate of Return (IRR)

The next step is determining the return on investment your investors will seek. The internal rate of return (IRR) required by investors will vary depending on the investor, the stage of the EdTech company they’re investing in (early-stage deals require higher returns than later-stage deals), and the industry trends.

Based on our experience, VCs typically look for a 40-60% IRR on the companies they invest in. Over the last few years, venture capital firms, on average, have generated a 19.8% IRR. Keep in mind that this is an average, so it includes their failed deals (the ones that went wrong) as well as their success stories. They look for a 40%-60% IRR because providing venture capital is a high-risk business, and an estimated 80% of the deals they invest in are unsuccessful or don’t live up to expectations.

In this example, I’ll use 40%IRR as a low-end and 60% IRR at the high-end expected rate of return.

Keep in mind that as your EdTech venture becomes more proven and successful, the perceived risk of the investment goes down, so investors will be willing to accept a lower IRR.

Calculating Your Post-Money Valuation

The next step is to calculate your Post-Money value. Let’s assume you are looking to do a Series A capital raise, so we will also assume investors will require a 40-60% IRR over the next five years.

Using these IRR assumptions, we discount the Exit Value back to its present-day value to estimate the post-money valuation of your business. The post-money valuation is your EdTech company’s value after receiving the infusion of capital. In contrast, a pre-money valuation is the value of your EdTech company as it is today, without the injection of capital.

Post-money valuation = Exit Value / (1 + IRR)^5

Post-Money Value = $12.3 million/(1 + 40%)^5 = $2,287,865

This is the high end of the post-money valuation range, based on the lowest expected rate of return.

To calculate the low end of the post-money valuation range, use the highest expected rate of return.

Post-Money Value = $12.3 million/(1 + 60%)^5 = $1,173,466

This means the post money value of your early-stage EdTech company is between $2.3 million to $1.2 million.

It’s interesting to note that while we calculated the Exit Value using a 4.6x multiple (from the publicly traded EdTech companies), the EV/Revenue multiple for your early-stage EdTech company is much higher and between 4.7 and 9.2 times your current revenues of $250,000.

Getting the Best Terms

Finally, remember that the post-money valuation arrived at above is for 100% of your business. When doing a capital raise, it’s important to raise as much capital as possible while giving up as little equity as possible in exchange.

To get the best terms from potential investors without giving up all your equity, your integrated financial model must include an accurate estimate of your operating expenses so you can figure out exactly how much capital you need.

If your projections show that you need $1 million in growth capital, you may be able to raise the capital you need and only give up 44% of the equity in your company ($1M/$2.3M=44%) in exchange.

The other important this you can do to limit the amount of equity you give to investors is to work with an experienced investment banker. An investment banker who knows the education space can help you build a compelling investment deck, create an integrated financial model backed by solid assumptions, and introduce you to more investors. The more investors you speak with and the more term sheets you receive, the better terms you’ll get.

About the Author and Jackim Woods & Co.

Rich Jackim is an education industry investment banker and educational industry entrepreneur, and former mergers and acquisitions attorney.

For the last 25 years, Rich has been providing boutique investment banking services to middle-market companies in the education sector.

Rich also founded a successful training and certification company called the Exit Planning Institute which he sold to a private equity group in 2012.

Rich is also the author of the critically acclaimed book, The $10 Trillion Dollar Opportunity: Designing Successful Exit Strategies for Middle Market Businesses.

Jackim Woods & Co offers skilled mergers and acquisitions advisory services to privately owned schools, colleges, and EdTech companies in both sell-side and buy-side transactions. Jackim Woods & Co has arranged over 100 successful transactions, ranging from less than one million to more than eighty million dollars in value.

If you own an education-related business and are interested in exploring your options, I would welcome an opportunity to speak with you. Feel free to contact me at 224-513-5142 or rjackim@jackimwoods.com.

Read More

2022 EdTech Valuation Multiples

2021 was a tough year for EdTech companies. Despite 2021 being another record year for investment in the EdTech sector, including high-profile IPOs for Duolingo, Udemy, Coursera, and Instructure, companies in the EdTech sector saw the value of their companies drop by as much as 40% in some cases.

In 2021 investors learned to take a more conservative approach to value EdTech companies after Udemy’s IPOs demonstrated that the public markets will not support crazy valuations. Udemy went public at a $4.0 billion valuation, but as of the start of 2022, its market capitalization was only $1.8 billion. Investors lost $2.2 billion by overvaluing Udemy. As a result, other EdTech companies like Coursera and Duolingo reduced their IPO valuations in 2021.

The sell-off of EdTech stocks in the second half of 2021, was largely fueled by concerns over lofty valuations, inflation, and rising interest rates. These same concerns also caused a sell-off that impacted all technology, software, and growth stocks.

2022 Public EdTech Valuation Multiples

Despite the sell-off, EdTech companies are still trading at generous valuations. The table below shows the valuation multiples for a representative sample of publicly-traded EdTech stocks that we track.

As the data above indicates, the valuation of EdTech stocks varies depending on who the end-user is (K12 & Higher Ed vs B2C & Corporate). B2C and Corporate EdTech stocks sell for a higher multiple than Higher Ed and K12 companies.

As of March 2022, the median multiple of revenues for public Higher Ed & K12 EdTech companies was 2.2x and the average was 3.3, while the median multiple for public B2C & Corporate EdTech companies was 5.7 and the average was 6.6x.

Overall, the median revenue multiple for the entire publicly traded EdTech sector was 2.4x and the average was 3.9x.

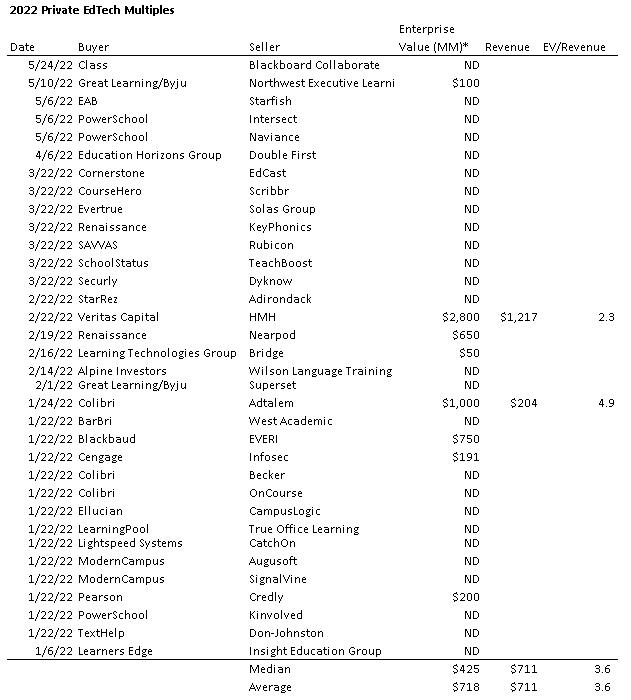

2022 Private EdTech Multiples

The selloff in the public markets also affected private EdTech multiples. The following table shows the 2022 private EdTech transactions Jackim Woods & Co tracks and the associated valuation data.

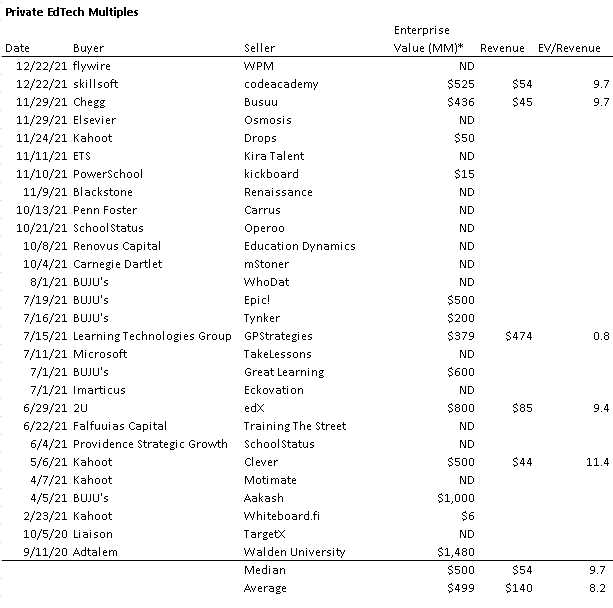

The following table shows similar data from 2021 when EdTech stocks experienced a COVID-related boost to their valuations.

A comparison of the data in the tables above shows that the median revenue multiple for private EdTech companies dropped from 9.7x in 2021 to 3.6x in 2022. Similarly, the average multiple of revenue for private EdTech companies dropped from 8.2x in 2021 to 3.6 in 2022.

2022 EdTech Private Company Valuation Multiples

Revenue multiples for private EdTech companies in early 2022 range between 2.0x and 5.0x, with a median of approximately 3.6x revenue.

Despite the macro conditions mentioned above, we expect the EdTech sector to continue to do very well in response to a growing global demand for new and better ways to deliver educational content from K12 to higher ed, to corporate training and lifelong learning.

As a result, we expect valuation multiples to remain strong for privately owned EdTech companies that are looking to raise growth capital or have a liquidity event. In addition, we expect that multiples for publicly traded EdTech companies will increase once inflation is under control.

About the Author and Jackim Woods & Co.

Rich Jackim is a mergers & acquisitions attorney, investment banker, and educational industry entrepreneur. In 2016 he founded the Exit Planning Institute, a very successful corporate training and certification company that he sold to a private equity group in 2012.

For the last 25 years, Rich has been providing boutique investment banking services to middle-market companies in the education sector.

Jackim Woods & Co offers skilled mergers and acquisitions advisory services to privately owned schools, colleges, and EdTech companies in both sell-side and buy-side transactions. Jackim Woods & Co has arranged over 100 successful transactions, ranging from less than one million to more than eighty million dollars in value.

If you are interested in exploring your options, I would welcome an opportunity to speak with you. Feel free to contact me at 224-513-5142 or at rjackim@jackimwoods.com.

Read More